The latest new lending data - a flow metric - from the ABS showed a slight slump in the value of owner occupier loans written in September, by 0.1% to just over $16 billion in seasonally-adjusted terms.

This was 8.4% than a year ago. Buoying the overall results was an uptick in investment lending, up 2% over the month and 2.6% over the year to $8.95 billion.

Looking at the stock metric - private sector credit growth - there was a continued slowing in the level of household debt in the system.

Annual growth was 4.9% in the year to September, the weakest result since August 2021 when Covid outbreaks were hitting Victoria and New South Wales.

Annualised housing credit growth was 4.2% - the weakest result since March 2021.

In that time, home prices have pretty much rebounded to sit just 0.5% below their peak, and CoreLogic expects a new peak in dwelling prices to happen mid-November.

Perth and Adelaide are already at fresh peaks after experiencing shallower troughs compared to their east coast counterparts.

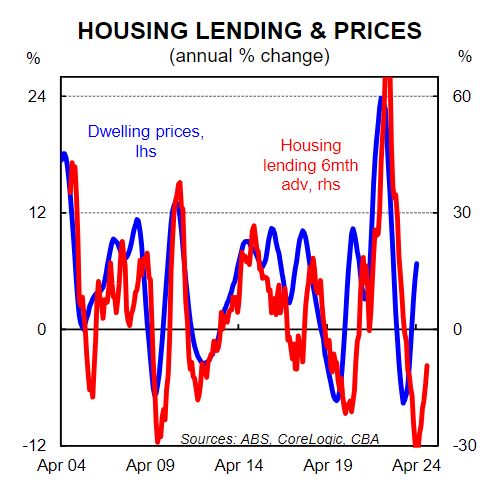

For years, strong lending figures generally ran toe-to-toe with strong dwelling price growth, however the two have seemingly decoupled through 2023.

CBA's head of Australian economics Gareth Aird explained why.

The usual relationship between new lending and home prices has broken down. Housing loan commitments have fallen by around 30% since May 2022," Mr Aird said.

"A decline of this magnitude would ordinarily be expected to be accompanied by an ongoing decline in home prices. But these are extraordinary times.

"Australia’s population growth has surged over the past year. And home building has not kept pace.

"As a result, vacancy rates have dropped to record lows in most capital cities and the rental market is hot. This has put upward pressure on home prices."

According to NAB, the ratio of new population per dwelling approval is now at 3.6, the highest it's been since the series began in 1984.

Foreign buyer uptick

A recent NAB survey of residential property professionals demonstrated lending to foreign investors hit a five-and-a-half year high.

"The share of total market sales to foreign buyers in new housing markets increased for the fourth straight quarter ... to 10.1% in the third quarter," NAB chief economist Alan Oster said.

"This was mainly due to noticeably higher activity levels in NSW, where market sales increased to 14.9% (9.2% in Q2) and Victoria where it also lifted to 11.3% (7.4% in Q2).

"In established housing markets, the share of foreign buyers rose to a 4-year high of 4.1% in Q3 and increased in all states led by Victoria (5.0%)."

ABS lending data released today shows there was $640 million written for 'non residents' in the September quarter, an uptick from $597 million in the previous quarter.

They borrowed on average $713,000, which is higher than resident averages.

"Put simply there is a supply/demand imbalance in the housing market. Potential entrants into the housing market and renters feel the impact of this mismatch most acutely," CBA's Gareth Aird said.

"Meanwhile many home borrowers with a mortgage are also feeling the pain of significantly higher mortgage rates."

Undersupply a persistent problem

Of the property professionals surveyed by NAB, 79% believe there's a supply-demand imbalance in their area, and all states' property professionals believed there was an undersupply.

As the Housing Industry Association noted, lending for new homes fell to a 20-year low in September, much lower than its 'GFC-level lows' espoused in recent months.

“There were only 4,282 loans issued for the construction or purchase of new homes in September, leaving the last three months 27.7% lower than during the same quarter last year,” said Tim Devitt, HIA senior economist.

“This slowdown in lending for new housing will make it increasingly difficult to reach the Australian government’s target of building 1.2 million new homes in five years."

Any hope for first home buyers?

The ABS reports there was a tick over $9.2 billion in loans written for owner occupiers in September.

This marks a slight increase from $9.16 billion in August, but is down markedly from the March 2009 high of $16.26 billion, and more recent highs of $16.3 billion in January 2021.

A recent first home buyer survey of 3,000 respondents by mortgage insurance provider Helia, formerly Genworth, highlighted the difficulties faced by the sector when it comes to a deposit.

Approximately 80% of respondents can't save the 20% requisite deposit for their target home to avoid paying lenders mortgage insurance.

The research noted it would take a median-earning couple saving 20% of their income 13 years to save a 20% deposit on a house in Sydney and eight years for that on an apartment in the city.

Around two in five require deposit help - 60% of that group gets all or part of it from their parents, while 29% have their parents act as guarantor.

Photo by Dmitry Osipenko on Unsplash